By Palak Devpura

How a $1.63 billion handshake collapsed in thirty-nine days, why a Bahamas-based shareholder broke the deal, and what every founder, fund and family office must learn from the strangest M&A story in Indian sport.

Two matches, one stadium

Tonight, at Sawai Mansingh Stadium in Jaipur, Riyan Parag will toss the coin against Gujarat Titans. Pink jerseys, floodlights, the giant screen, the noise that makes the air shake. The game most of India will be watching is the one with bat and ball.

There is another game underway. It has no scoreboard, and it is being played in offices in Mumbai, courtrooms in London, family-office desks in Phoenix and Mumbai, and a bench at the Bombay High Court that has, in the last six weeks, twice issued notice to a UK-incorporated company called Emerging Media Ventures. The number on this game is one-and-a-half billion US dollars and change. The clauses being argued over are exclusivity, indemnity, and a tiny line of Indian company law called Section 241 that has, quietly, broken a deal that was supposed to be the largest in IPL history.

If you want to understand modern Indian dealmaking — the kind that runs through Mauritius and London and the NCLT and the BCCI all at once — this story is your textbook. The first match will be over by midnight. The second one is mid-innings, and is going to run for years.

Where the cap table came from

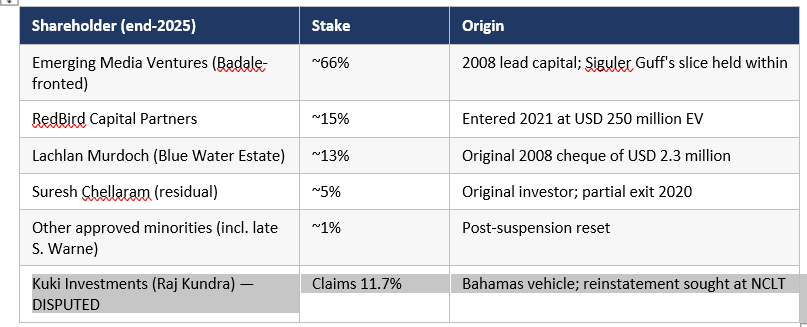

$67 million and other ancients numbers

In April 2008, when the BCCI auctioned off the eight original IPL franchises, Rajasthan was the cheapest team on the board. Mumbai sold for USD 111.9 million. Bangalore for USD 111.6 million. Most of the others lived in the seventies and eighties. Rajasthan went for USD 67 million to a UK-incorporated entity called Emerging Media Ventures, fronted by a British-Indian entrepreneur named Manoj Badale and sitting inside a London technology group called Blenheim Chalcot.

What few people noticed at the time was the cap table that came with the cheque. Lachlan Murdoch, the eldest son of Rupert, wrote a personal cheque of USD 2.3 million for roughly thirteen percent — held through a vehicle called Blue Water Estate. A Nigeria-based Indian businessman, Suresh Chellaram, took five percent through Kelowna Investments. Tresco International came in alongside. The Indian operating company, then called Jaipur IPL Cricket and later renamed Royals Multisport, sat in Mumbai. The chain ran Mumbai-up-to-Mauritius-up-to-the-United-Kingdom. International from the first day.

In 2009, RR became the first IPL franchise to publicly sell a stake. Bollywood’s Shilpa Shetty and her husband Raj Kundra bought 11.7 percent through a Bahamas-incorporated entity called Kuki Investments. Cameras everywhere. Brand value soaring. For two years, it looked like a marketing coup.

Then came 2013. Spot-fixing, a betting scandal, three RR players arrested, and an investigation that travelled all the way to the franchise’s own ownership. By 2015 the Lodha Committee had banned Kundra for life and suspended the team for two seasons. On paper, Shetty and Kundra exited. The word “exited” will, in 2025, become a litigated word.

Between 2018 and 2025 the cap table grew up. Emerging Media bought back the Chellaram stake in 2020. RedBird Capital — the same American sports private-equity outfit that holds positions in Liverpool FC and the Boston Red Sox parent — entered in June 2021 with about USD 50 million for fifteen percent at a USD 250 million enterprise valuation. Siguler Guff, a USD 18 billion private-markets firm, took a sub-ten-percent slice held within Emerging Media’s tier. Shane Warne was reportedly granted a small stake before his death in 2022. By the end of 2025, the structure that the Somani consortium would later try to buy looked like this:

Two numbers from that table are worth pausing on. Lachlan Murdoch’s USD 2.3 million was, on the original Somani offer, going to come back as roughly USD 210 million. A 92x return on a single ticket. RedBird’s USD 50 million was set to come back as roughly USD 200 million — a clean 7.8x. These are returns most private equity funds will not produce in a lifetime.

And then there is the line at the bottom. The disputed line. The line that detonated everything.

Where the deal began to fail

The thirty-nine days

On 25 March 2026, a deal was announced. A consortium led by Arizona-based entrepreneur Kal Somani — joined by Walmart heir Rob Walton (principal owner, NFL Denver Broncos) and Sheila Ford Hamp (principal owner, Detroit Lions), along with her son Michael Hamp — would buy 100 percent of Rajasthan Royals for USD 1.63 billion. They had outbid Avram Glazer (Manchester United co-owner, through Lancer Capital), Capri Group, the Aditya Birla Group, and the Times of India Group. They were the lead bidder through more than one round of binding bids.

Thirty-nine days later, on 3 May 2026, the seller signed a definitive agreement with somebody else.

To understand what happened in those thirty-nine days, you need to understand a single page of the term sheet that almost nobody reads in detail. The exclusivity clause.

An exclusivity clause does one simple thing: it stops the seller from talking to anyone else for a defined window. Inside that window, the buyer locks down due diligence, finalises its consortium structure, raises its capital, and produces binding documents. Every word inside the clause matters. Was the no-shop a hard one, or did the seller have a fiduciary out? Did exclusivity auto-extend on a regulatory delay, or did it terminate cleanly on a missed milestone? Was there a break fee — a cheque the seller pays to the buyer if it walks away? Was there a funded-commitment milestone — a date by which the buyer’s consortium must deliver signed equity commitment letters from each member?

“In M&A, the price is the headline. The exclusivity clause is the deal.”

From everything in the public record, the answer to the funded-commitment question is the answer that broke the Somani deal. Reports indicate the Somani group walked into the exclusivity window with strong-interest letters from co-investors, not signed equity commitment letters with hard conditionality. The names were big. The cheques were not yet binding. Somani approached additional large investment firms inside the window. Commitments did not materialise on the seller’s timeline. Somani also reportedly pushed for a majority position within his own consortium, but the precise contributions of his co-investors stayed unsettled.

The seller, almost certainly, had reserved itself an off-ramp. A milestone-based exclusivity with a clean termination right on missed milestones is now standard market practice in Indian competitive auctions. If the buyer cannot produce funded commitments by Day X, exclusivity lapses automatically and the seller is free to negotiate in parallel. The two-percent premium of the eventual Mittal–Poonawalla bid (USD 1.65 billion against USD 1.63 billion) and the speed at which it was signed both suggest that a parallel option was already in advanced shape — which is itself only possible if exclusivity had either lapsed or contained a fiduciary-out carve-out the seller could legitimately invoke.

This matters because the Somani consortium has now publicly disputed the framing that they “withdrew.” They say they were ready to close. They are reportedly preparing a legal notice to RR management and to the BCCI alleging deliberate procedural delay during exclusivity. If that notice converts into a claim, the question becomes: where, and how, would they sue?

My read is that they have three forums and none of them is friendly. An Indian civil suit in the Bombay High Court would be slow, would face strong defences on the seller’s milestone rights, and would expose the Somani group’s own commitment letters to discovery — which the Somani side may not want. English courts, given Emerging Media’s UK incorporation, are more accessible, but English commercial courts apply contract terms strictly: if the term sheet says “milestones missed, exclusivity ends,” English courts will read it that way. ICC arbitration only opens up if the term sheet contains an arbitration clause, which is unusual at the term-sheet stage but not unheard of in sophisticated multi-party deals. The most realistic outcome of a Somani notice is not litigation but a face-saving settlement — perhaps a mutual non-disparagement and a quiet release.

Where the title risk lives

The Bahamas route

While Somani was failing to close, a parallel battle was being fought over a stake that, on paper, no longer exists.

In 2025, Raj Kundra — through Kuki Investments, the same Bahamas vehicle that had bought into RR in 2009 — filed a company petition before the National Company Law Tribunal in Mumbai under Sections 241 and 242 of the Companies Act, 2013. The allegations: oppression and mismanagement, siphoning of funds, related-party transactions executed without disclosure, and non-maintenance or fabrication of statutory records. The remedy sought: reinstatement of the 11.7 percent stake.

The seller’s response was unusually aggressive. Rather than fight the petition on its merits in Mumbai, Emerging Media Ventures went to the High Court of England and Wales and, on 29 January 2026, obtained an ex parte anti-suit injunction. The order restrained Kundra and Kuki Investments from pursuing the NCLT proceedings, or initiating any India proceedings, against Emerging Media.

An anti-suit injunction is a particular kind of order. It does not bind the foreign court directly. It binds the party — in personam. If the party defies it, the issuing court can hold the party in contempt, freeze assets within its jurisdiction, and refuse to enforce any foreign judgment they obtain. UK courts have been comfortable issuing them for decades. Indian courts have generally not.

Kundra moved fast. On 24 March 2026 — one day before the Somani deal was publicly announced — he approached the Bombay High Court under Clause XII of the Letters Patent and asked for an anti-enforcement order. His pitch was simple. He resides in Mumbai. The Indian operating company is registered in Mumbai. The alleged oppressive acts concern an Indian company. The NCLT is in Mumbai. A substantial part of the cause of action arose in Mumbai. Therefore the Bombay High Court has the jurisdiction to declare that the UK injunction does not run within India.

Justice Ahuja granted leave. In a separate hearing, Justice Milind Jadhav noted that an arguable case had been made and issued notice to Emerging Media Ventures. The Court characterised the English order as potentially “non est, violative of principles of natural justice and unenforceable.”

“A foreign anti-suit injunction cannot bury a shareholder’s statutory right to file an oppression petition. Indian courts have now made that clear.”

My view, having watched Indian courts handle the comity question for the better part of two decades, is that the anti-enforcement order is more likely than not to be granted. The right to invoke Sections 241 and 242 is a core piece of Indian shareholder protection. Indian courts have repeatedly held that statutory remedies of this kind cannot be ousted by foreign injunctions, contractual choice of forum, or even — in the limited class of non-arbitrable disputes — by arbitration agreements. An ex parte order, granted without hearing the affected party, is treated with particular suspicion in any natural-justice analysis. If the Bombay High Court does grant the anti-enforcement order, the UK injunction becomes a paper tiger inside India: it will continue to bind Kundra in jurisdictions where the UK order can be enforced (mostly common-law commercial centres), but it will not stop the NCLT petition from proceeding to hearing.

Which raises the deeper question for any buyer. Can the Mittal–Poonawalla consortium acquire clean title in a company whose controlling holding entity is currently defending a live oppression petition?

The answer is yes, but only with the right contractual architecture. In a transaction of this size, three layers of protection are essential. A specific indemnity from the seller, uncapped or capped at a high multiple of the disputed stake’s pro rata value, covering all costs, settlements, judgments, and re-issuance of shares arising from the Kuki claim. An escrow holdback equal to the value of the disputed 11.7 percent (so roughly USD 190 million on a USD 1.65 billion deal), released only upon final disposal of the NCLT proceedings or a written settlement. And, ideally, R&W insurance with a specific policy carve-in for the Kundra matter — pricier than usual, but available in this market. A sophisticated buyer also negotiates a step-in right to control the litigation, since a buyer’s appetite for settlement is often higher than the seller’s. Without all three of these, no rational buyer should close.

And the optimal off-ramp for Kundra himself? Litigating an oppression petition through to a final order takes years and produces uncertain reliefs. The cleanest exit, and the one I would push for if I were on either side of the table, is a negotiated buy-out at an agreed valuation — almost certainly at a discount to the 11.7 percent of the headline transaction value, with a public release of all claims, no-admission language, and an undertaking not to write to BCCI again. Money settles most disputes. This one will too.

Where the deal closed

Why the Mittals walked in

On 3 May 2026, the seller signed with the Mittal family — Lakshmi Niwas Mittal, his son Aditya, and his daughter Vanisha Mittal-Bhatia — together with Adar Poonawalla, the CEO of Serum Institute of India. The price was USD 1.65 billion, a marginal premium over Somani’s USD 1.63 billion. The new cap table on completion: Mittal family roughly 75 percent, Poonawalla roughly 18 percent, approved existing investors including Manoj Badale roughly 7 percent. Badale stays on as a “bridge.” The buyer-side advisors were Latham & Watkins, Cyril Amarchand Mangaldas, Trilegal, and Goldman Sachs.

Three things made this deal closeable when the other one was not. The capital was domestic, anchored, and unambiguous — there was no funded-commitment risk because the Mittals and Poonawalla wrote their own cheques. Founder continuity was protected, which the Somani group had refused to do. And the buyer walked into the Kundra exposure with eyes open and the kind of advisory bench that does not get built unless the intent is to actually close.

The transaction is now subject to BCCI approval, IPL Governing Council approval, Competition Commission of India clearance, and other regulatory consents. Of these, the BCCI gate is the most interesting one. Under the IPL Operational Rules, a change of control requires sport-governance approval. There is no express duty under those rules to assess title risk before approving the transfer. But Kundra has formally written to the BCCI urging it to withhold approval on exactly this ground. Whether the BCCI develops a soft duty here — a due-diligence step on pending company-law claims against the holding entity — will, I suspect, be one of the quiet legacies of this deal. It should. A franchise transfer where the controlling entity is the respondent in a Section 241 petition is a transaction the regulator ought to look at twice.

The CCI side of the gate is, by contrast, the well-trodden one. There is no horizontal overlap of the kind that triggers the deepest scrutiny — Mittal does not own another IPL franchise, and Poonawalla’s interests sit elsewhere. The filing will lean on a careful market-definition argument and on the structural absence of foreclosure concerns. Expect approval, but expect it to take its time.

Where the structure pays the price

The trap door in the offshore stack

There is a line in the Income-tax Act, 1961, that very few sports journalists know about, but every cross-border lawyer thinks about every day. Section 9(1)(i), read with Explanations 5, 6 and 7. The indirect-transfer regime.

Translated into plain English: if a non-resident transfers shares of a foreign company that derives, directly or indirectly, its value substantially from assets located in India, the transfer is deemed to take place in India and the resulting capital gains are chargeable to Indian tax. The threshold under the Explanations is broadly that more than fifty percent of the foreign company’s value is attributable to Indian assets, and the Indian-asset value crosses ten crore rupees. A franchise valued at USD 1.65 billion, with effectively all its value sitting in the Indian operating company, easily clears both thresholds.

READ: Kal Somani buys Rajasthan Royals for $1.63 billion (

Which means that when ownership of Royals Multisport changes hands, the exit at any tier of the offshore stack — Bahamas, Mauritius, the United Kingdom — that is selling shares in a foreign holding entity whose value is substantially Indian, may itself be a taxable event in India. The Indian buyer, by extension, has withholding obligations under Section 195. If the buyer fails to withhold, it becomes liable as an assessee-in-default, plus interest and penalty. This is not theoretical. This is exactly how the Vodafone story began, and exactly why every cross-border M&A SPA in India in 2026 contains a long, technical Section 9 indemnity from the seller and a careful withholding-mechanics annexure.

Which leads to a question that every founder routing capital into India should ask themselves in 2026. Is the cross-border holding stack — UK to Mauritius to India — still optimal?

My answer, based on what I am seeing across deals over the last eighteen months, is no. Not for new investments. The traditional offshore wisdom was built on a tax-treaty arbitrage that has been progressively closed, and on a regulatory environment in India that has, correctly, become more sceptical of layered offshore structures. The GIFT City fund route — IFSC-regulated category I and II AIFs, with their own tax preferences and a regulatory regime designed for cross-border investment into India — has matured to the point where it is, for many tickets, the cleaner answer. The closing-timeline advantage alone (two-to-four weeks against the traditional forty-five-to-sixty days for a Mauritius-routed transaction) is decisive in competitive deals. I have spent the last year moving clients toward GIFT City structures. The Rajasthan Royals story is, among many other things, a reminder of why.

Where this market goes next

The next two billion

The Royals deal is not happening in isolation. The Royal Challengers Bangalore franchise was sold this year to a Birla and Times-led consortium for roughly USD 1.78 billion. Two transactions in the USD 1.6 to 1.8 billion band, inside a single window. This is no longer noise. It is a market.

What is the methodology? Three things, layered. First, a sustainable EBITDA multiple — IPL franchises now produce real, repeating cash flows from media-rights distributions, sponsorships, ticketing, merchandise, and the increasing global syndication of the format. Apply a sports-market multiple (currently in the high-single-digits to low-teens for premium global franchises) and the math gets you part of the way. Second, a media-rights-share NPV — the BCCI’s central media rights pool grows roughly with India’s screen economy, and each franchise’s share is a discounted future stream. And third — most importantly — a scarcity premium. There are exactly ten IPL franchises. There will not be twenty. American sports valuations have taught the world what scarcity does to price. India is now learning the same lesson, in compressed time.

Which raises the most interesting question of all. With American capital actively bidding for Indian sports franchises — Walton, Hamp, Glazer, RedBird already invested — does it now make sense to build a regulated cross-border investment vehicle for Indian sports, parallel to the GIFT City fund structures used for Indian tech?

My view: yes, and somebody will build it within the next eighteen months. The deal-flow will originate from three pools. US sports family offices (the Walton, Ford-Hamp, Kraft, and Lurie kinds of money), looking for international sports diversification at a moment when domestic franchise valuations have plateaued. NFL and NBA owners’ personal vehicles, which are increasingly bypassing institutional fund structures and writing direct cheques into international sport (the Detroit Lions principal is on the consortium list precisely because of this trend). And institutional sports private equity (RedBird, Arctos, Ares Management Sports), which has spent four years building an India thesis and is now looking for repeatable structures rather than bespoke deals. A GIFT City-domiciled sports infrastructure fund — with the right SEBI registration, the right tax preferences, the right India-onshore vehicles, and the right regulatory comfort with the BCCI — is the natural answer.

That fund does not exist yet. It will. And when it does, the second match in the cricket stadium — the one without a scoreboard — will become the first match for a generation of investors who, today, still think that IPL is a sport.

Coda

The clause nobody read

Twenty-five years of practice teach you a few things. They teach you that the boring clauses decide everything. They teach you that bid magnitude is not bid bankability — a smaller bid that closes is worth more than a larger one that does not. They teach you that funded commitment letters are not optional. That cross-border holding stacks come with cross-border vulnerabilities. That the NCLT is a powerful forum and underestimating it is expensive. That foreign anti-suit injunctions cannot bury Indian statutory rights. And that founder continuity — undervalued by most investors — quietly closes more deals than any number on a spreadsheet.

There is one other lesson, and it is the one I find myself returning to most often when I sit across the table from a founder who has just received a marquee term sheet. Optionality is a finite resource, and exclusivity spends it. Every day inside an exclusivity window is a day during which the seller is poorer than it was the day before. Outside money has stopped circling. Other bidders have moved on.

The market reads exclusivity as a deal that is going to close. When it does not close, the seller emerges weaker than when it entered — slower, less leveraged, with a story that needs explaining. The Rajasthan Royals seller managed this risk well, by all appearances, because somebody on the sell-side had drafted milestones into the exclusivity letter and held the buyer to them. Not every founder is that lucky. The cleanest protection a seller can give itself is a milestone-driven exclusivity with a clean termination right and, where the buyer demands deeper lock-out, a properly priced break fee. The cleanest protection a buyer can give itself is to never enter exclusivity with anything less than signed equity commitment letters from each consortium member. Both sides forget this. Both sides should not.

Riyan Parag’s coin will land in a few hours. The Royals will play, and probably win. The crowd will go home happy. And somewhere, in Mumbai or London or Phoenix, a lawyer will be drafting the indemnity clause that decides whether tonight’s match was the last one played by this version of the Rajasthan Royals — or merely the first of many played by the next.

In the second match, the one without a scoreboard, the innings are still being bowled.

Palak Devpura is the founder of Spinach Laws. For more legal analysis and updates, subscribe to The Legal Edge by Spinach Laws newsletter on LinkedIn.